I've been re-reading Adam Tooze's Crashed and so much is relevant. Today, central bank liquidity swaps.

During the financial crisis, the dollar funding needs of foreign banks (in particular European banks) would have quickly overwhelmed the foreign exchange reserves of their home-country central banks. To deny these commercial banks liquidity assistance could have been disastrous, but lending to the most fragile foreign banks without adequate collateral would have exposed the Federal Reserve to significant risk. As a solution, the Fed provided liquidity assistance to international banks through swap lines set up with other central banks. They were not a new invention in 2007, but the Fed used them on an unprecedented scale.

Tooze writes

“from 2007 the Fed repurposed an instrument that was first developed in the age of Bretton Woods. To manage the fixed currency system in the 1960s the central banks had developed a system of so-called currency swap lines that allowed the Fed to lend dollars to the Bank of England against a reverse deposit of sterling in the accounts of the Fed. Having gone out of use in the 1970s, the swap lines had been briefly revived in 2001 to deal with the aftermath of 9/11. In 2007 faced with the implosion of the transatlantic banking system, they were repurposed and expanded on a gigantic scale to meet the funding needs not of sovereign states but of Europe's megabanks." (p. 209-210)

The total amount outstanding on these dollar swap lines peaked at over $580 billion in December 2008, with over $310 billion outstanding with the European Central Bank. The swap lines prevented a euro-dollar or sterling-dollar crisis. “What the Fed had done for money markets, the central banks now did for the global provision of dollar bank funding. They absorbed the currency mismatch of the European bank balance sheets directly onto their own accounts.”

At the start of the financial strains due to the coronavirus pandemic in February 2020, the Federal Reserve had standing swap arrangements with the central banks of Canada, England, Europe, Japan, and Switzerland. On March 19 it added temporary arrangements with the central banks of Australia, Brazil, Denmark, Korea, Mexico, New Zealand, Norway, Singapore, and Sweden.

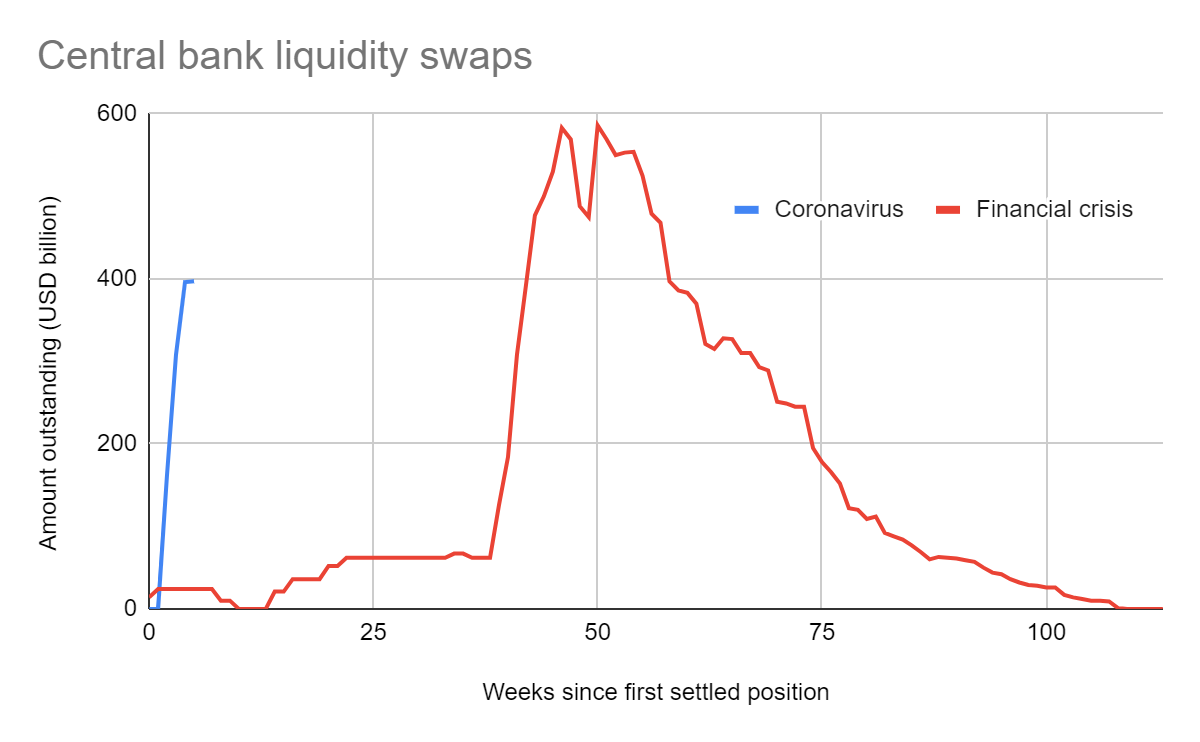

As of April 9, 2020, over $396 billion was outstanding. Three charts, using data from the New York Fed, and thoughts below.

Figure 1: This crisis struck funding markets much more quickly than the 2007-08 crisis.

The rush to use the swap lines is not a surprise. As we’ve seen with unemployment claims, equity markets, restaurants/bars/barber shops/etc., things have shut down jarringly fast.

Figure 2: Same data, but starting from the first week with greater than $100 billion in outstanding positions.

The peak is significantly lower this time around, at least so far. If it remains lower, I wonder if the lower dollar funding needs are more a result of crisis-specific factors or longer-term structural changes. A crisis specific factor could be the lower need for dollar liquidity on commodity/trade/shipping finance due to lower overall demand as a result of the pandemic, which is much more of an exogenous shock than the financial crisis. Longer-term changes could be a lower utilization of dollars in inter-regional trade payments (79.5 percent in 2016), cross-border payments intermediated through SWIFT (40 percent in 2019), or FX reserves (62 percent in 2018). At a first glance, none of these seem to have shifted enough since 2008 to explain the lower level of swap utilization today. Other structural changes are the US share of global production or trade. These levels are down about a percentage point, to around 15 percent of GDP, 14 percent of exports, and 18 percent of imports. So my initial assumption is that the lower swap line utilization today is mostly a result of crisis-specific factors.

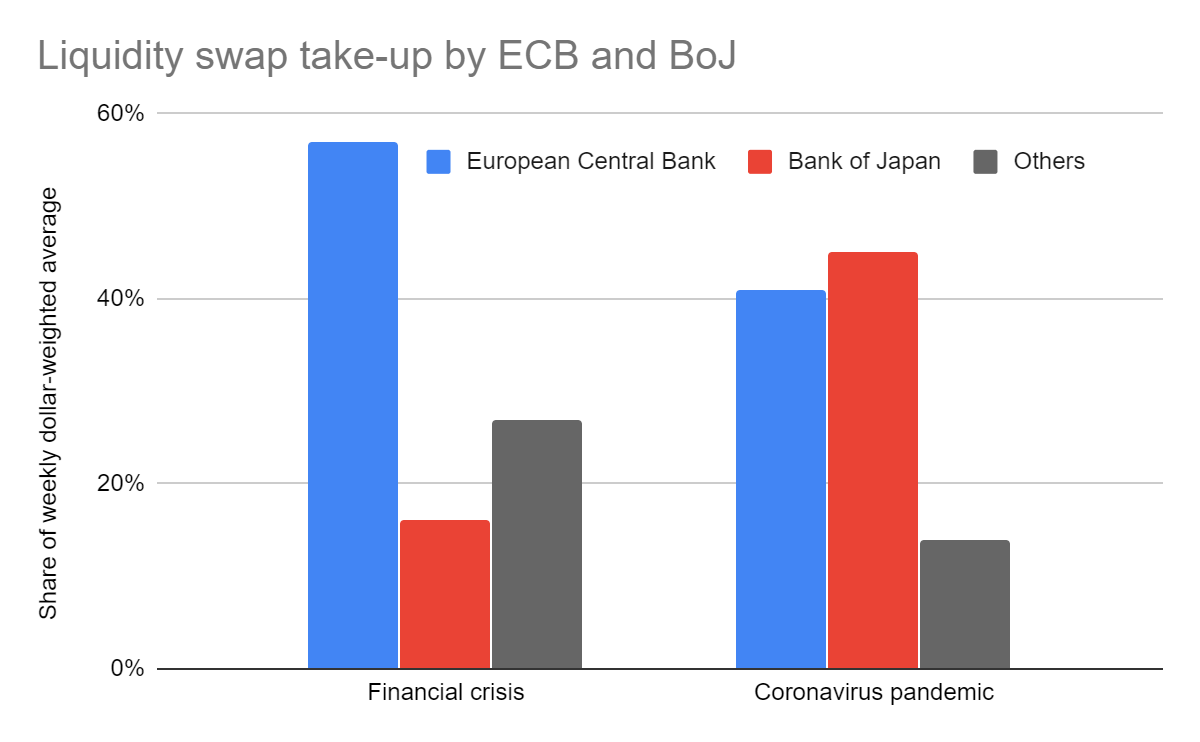

Figure 3: There has been a big shift in the relative amounts of swap lines utilized. The Bank of Japan has replaced the European Central Bank as the biggest user of dollar swaps this time (admittedly on just a few weeks of data so far).

The work of Iñaki Aldasoro, Torsten Ehlers, and Egemen Eren of the BIS provides an explanation:

“A striking fact is that non-US global banks have diverged in the size of their dollar assets as well as their dollar sources and uses since the Great Financial Crisis (GFC). This contrast is particularly stark between European and Japanese banks. Between 2007 and 2017, global dollar assets of Japanese banks increased by 88%, while those of European banks shrank by 42%. While Japanese banks increased their involvement in traditional banking activities, European banks have significantly shortened maturities of both their assets and liabilities, and shifted their business models to short-term arbitrage activities. These shifts have also led to differences in the demand for dollar funding.”

The authors explain that

“The divergence of activities between Japanese banks and European banks could be attributed to several reasons, such as the eurozone crisis, different levels of interest rates and hence the attractiveness of dollar banking, differences in bank supervision, among others.”So it comes back to questions about the eurozone, interest rates (policy, market, and natural), bank regulations, and more.. But that's it for now -- will be checking this data for updates (and, as a semi Swede, to see whether the Riksbank ends up using a swap line).

No comments:

Post a Comment